EV battery producers based in China, South Korea and Japan have nearly full control of the worldwide market and it’s not transforming whenever quickly.

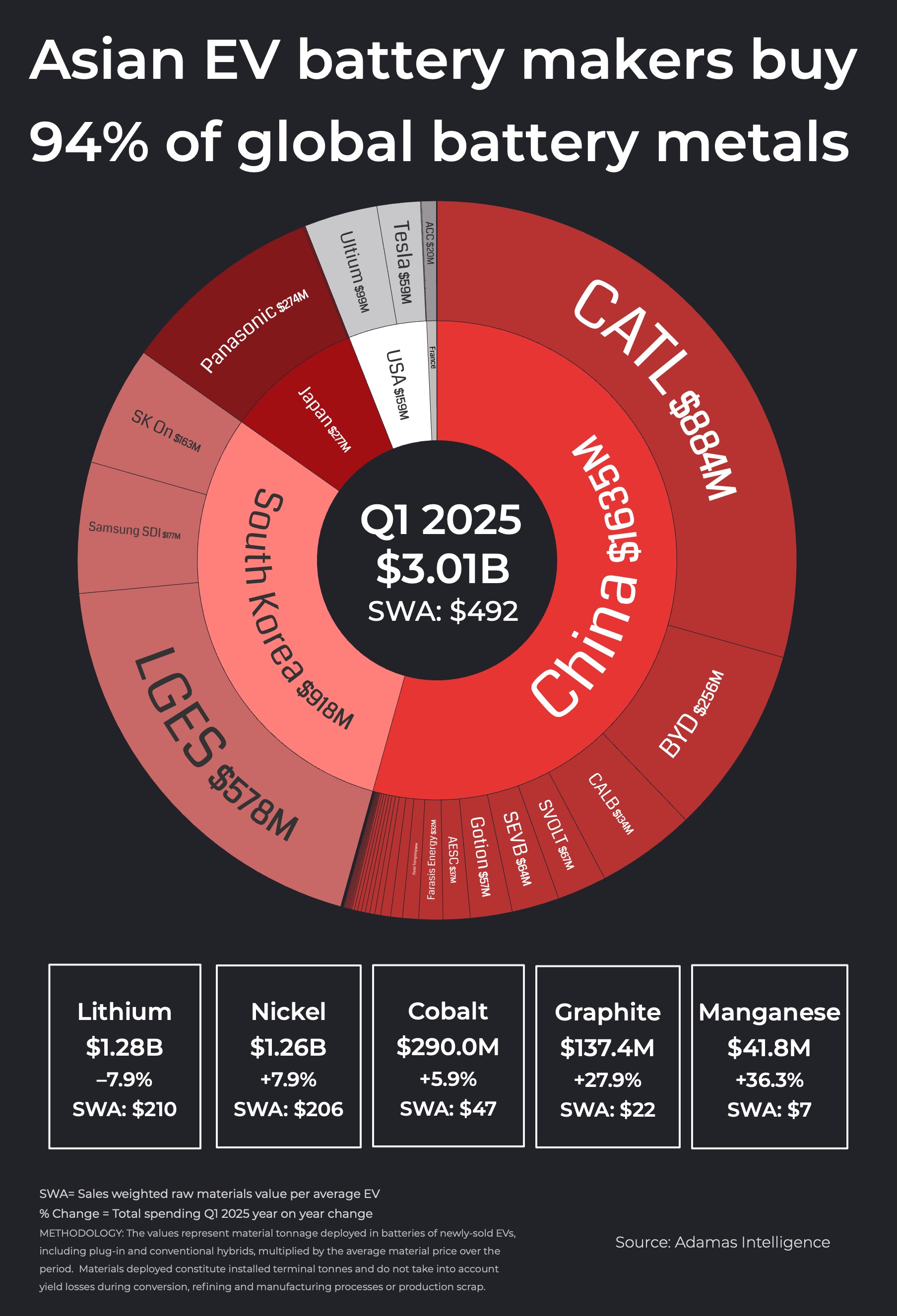

Throughout the very first quarter of 2025 a mixed $3.01 billion well worth of battery steels were had in the packs of freshly marketed EVs worldwide, up a moderate 1.3% year over year.

The stationary prices of the EV steel basket is fantastic information for cell providers and battery producers as need for basic material remains to expand. The tonnes of graphite, lithium, nickel, cobalt and manganese released throughout the very first 3 months was up a durable 27% year on year to a mixed 428.2 kilotonnes, according to information from EV supply chain research study professionals Adamas Knowledge.

Bearing in mind that the mounted tonnage does not think about any kind of losses throughout handling, chemical conversion or battery manufacturing scrap (typically well right into dual figure portions), so needed tonnes and earnings are meaningfully greater at the mine mouth.

The going along with chart reveals the investing of the greater than 60 worldwide cell providers and battery producers by nation of possession. It’s basically an all-Asia event with Chinese, South Oriental and Japanese battery manufacturers standing for 94% of basic material investing. EV batteries are a specifically leading hefty market with the huge 4– CATL, LGES, BYD and Panasonic– accountancy for 2 out of every 3 bucks invested.

Leading spender in The United States and Canada, Ultium Cells, is a fast-growing collaboration in between LG Power Service and General Motors, so practically a part of the battery supplier’s investing can likewise be designated to the East, making the supremacy of Oriental gamers a lot more widespread.

Additionally, because lithium iron phosphate or LFP’s market share in China has actually been over 50% right component of 3 years and leading EV manufacturer BYD has actually time out of mind transferred to an all LFP align, battery providers there under invest their NCM-reliant rivals by decreasing invest in costlier nickel and cobalt. That suggests on a mixed battery ability released basis their control of the marketplace is a lot more significant.

Nonetheless, Chinese battery manufacturers invest over half the worldwide total amount (Japan’s various other EV battery champ, AESC, is bulk possessed by China’s Envision team). Panasonic’s 9% market share in buck terms is greater than for overall battery ability released (6% in Q1 on GWh terms, according to Adamas) as a result of the big percentage of its cells winding up in traditional crossbreeds where nickel steel hydride is the cell of option and LFP has actually made no invasions.

In spite of its currently looming existence on the market, CATL, fresh from a smash hit share offering in Hong Kong, is boldy seeking development. The existence outside China of the Fujian-based firm, which in its existing type was just developed in 2011, is readied to increase quickly– as is the fostering of LFP cathode chemistries.

CATL currently has a footing on Western markets with its biggest operating plant outside China situated in Thuringia, Germany. A gigantic 100 GWh manufacturing facility presently unfinished in Debrecen, Hungary with the ability of gearing up as lots of as 1.5 million EVs annually, is readied to begin in the direction of completion of the year, and prepare for a 50 GWh center in Zaragoza, Spain are much progressed. All 3 manufacture LFP cells.

Battling control from the incumbents has actually been sluggish. The globe’s second car manufacturer, Volkswagen’s PowerCo, has yet to take into manufacturing any one of its prepared (and downsized) battery plants, the biggest of which lies in Ontario, Canada. Premier Ford’s BlueOval center making use of CATL’s LFP innovation is readied to begin manufacturing following year, yet offered the profession stress in between Washington and Beijing, the Chinese titan’s participation might be decreased better.

Tesla’s enthusiastic strategies to come to be a battery supplier in its very own right likewise appear to have actually struck a wall surface, with its Austin, Texas manufacturing facility standing for just 15% of overall basic material tonnes had in Tesla versions marketed throughout the very first 3 months of the year. Worldwide, Tesla stays CATL’s top client.

While France’s ACC, component possessed by Stellantis and Mercedes-Benz is worthy of an honourable reference, the $8 billion failing of Europe’s fantastic battery hope– Northvolt– reveals the advantages of economic situations of range and institutional understanding in the still fast-growing EV market.

In addition to that, China’s hold on the mine to megawatt pipe gives the bases of its ongoing supremacy.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/chart-asian-ev-battery-makers-buy-94-of-global-battery-metals/