At the beginning of the year cobalt rates was up to their most affordable degree ever before on a rising cost of living readjusted basis and gotten to near years lows nominally.

A rise in supply from the Congo, in charge of 80% of the globe’s cobalt result, combined with lukewarm need from the electrical lorry market, saw cobalt sulphate going into the EV battery supply chain in China be up to approximately simply $3,556 per tonne in January. That contrasts to a height of almost $19,000 a tonne in 2022.

Copper manufacturing in the DRC, with a large portion possessed by Chinese business, was increasing quickly– bring about a close to 40% enter the nation’s co-product cobalt result in 2024, however in February the nation revealed a 4 month restriction on exports to reduce the excess.

Cobalt sulphate rates properly reacted, leaping greater than 60% in March to balance $5,767 a tonne, and keeping the majority of those gains in April.

Cobalt result result is additionally boosting in Indonesia as its nickel deliveries swelled and the DRC is now in talks with the Asian nation to work together on handling supply of cobalt consisting of making use of allocations.

Cobalt intake in EV batteries surpassed various other resources of need like aerospace numerous years earlier and the influence of the DRC technique has actually been speedy.

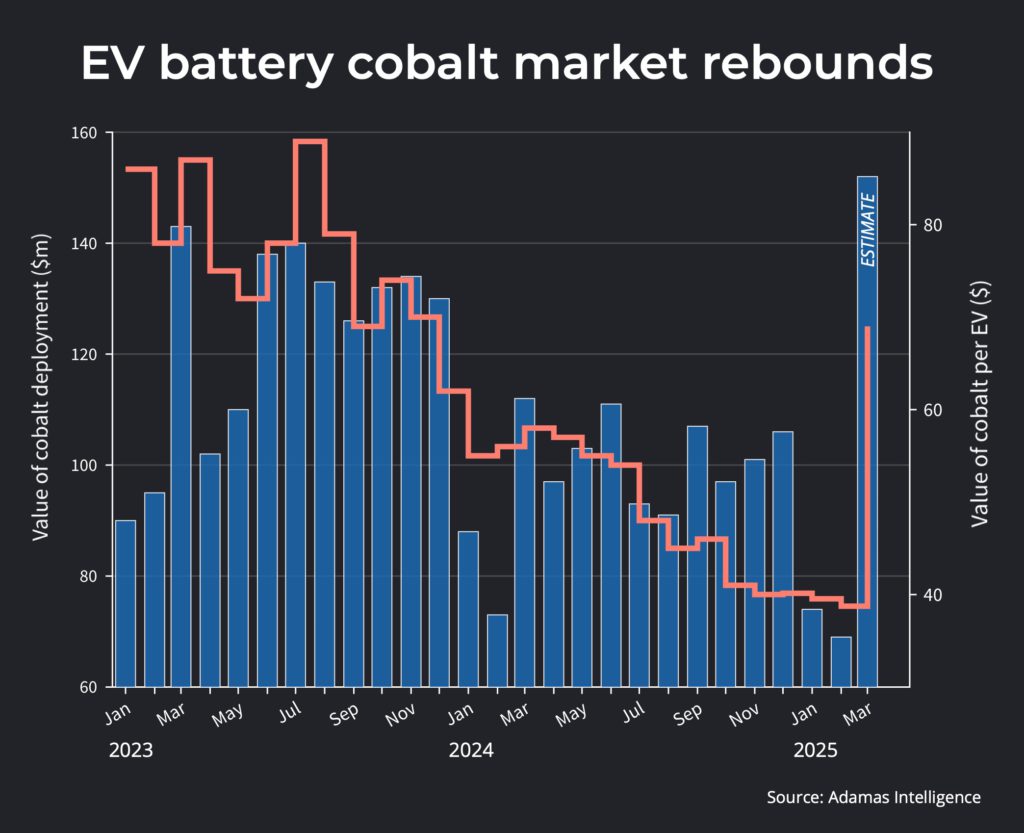

The most recent information from Adamas Knowledge tracking EV battery steel release in over 120 nations coupled with month-to-month rates reveals the cobalt market bouncing back right into life.

The approximated dimension of the battery cobalt market soared in March to a total $152.4 million, up 120% over February and the highest possible considering that December 2022, raising the worth of sales weighted ordinary cobalt included in tandem.

While March was a great month throughout the board for the EV market and by expansion battery steel release, and January and February are typically silent months for traveler lorry sales, cobalt greatly exceeded various other battery steels.

Nickel climbed by an extra suppressed 41%, additionally amidst increasing rates, while the worth of battery lithium release raised by 28% month over month, depending on increasing EV sales in Asia greater than rates, which are still bobbing along near all-time low of the cycle.

And while rate can make all the distinction for providers to the EV battery market, longer term fads for cobalt (and its ternary cathode relatives) in the EV market are much less motivating.

Lithium iron phosphate or LFP batteries remain to quickly take market share from NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminum) cathode chemistries.

The China-fueled surge of LFP has fostered a large divergence in international intake development prices of essential battery steels, according to Adamas Knowledge information.

For instance, in schedule 2024 iron and phosphorous release were up by 54% and 49%, specifically, for a consolidated 399.1 kilotonnes included in the batteries of offered EVs throughout the year.

On the other hand, international nickel release right into EV batteries raised 11% to 322.7 kt while that of manganese climbed 10% to 73.6 kt and cobalt 7% to 59.6 kt as the market remains to second hand the steel. Remembering that the set up tonnage does not consider any type of losses throughout handling, chemical conversion or battery manufacturing scrap (usually well right into dual number percents) so necessary tonnes are meaningfully greater at the mine mouth.

In overall, set up tonnage of nickel, cobalt and manganese in 2014 stood for 21% of the battery steel basket.

That’s below a 24% share in 2023 and 36% in 2020 when leading EV manufacturer BYD changed to an all-LFP line-up, and LFP-powered Tesla Design fours re-ignited uptake of the Ni-Co-Mn-free battery chemistry.

The globe’s biggest EV battery manufacturer CATL, in charge of 30% of complete battery ability released internationally in GWh terms, in April revealed that industrial manufacturing of sodium-ion packs will certainly start prior to completion of 2025. Because of its integral restrictions, sodium-ion is more probable to consume right into LFP’s market than NCM’s.

At the very least there’s that.

For a fuller evaluation of the EV battery steels market check out the May problem of The Northern Miner print and digital editions.

* Frik Els is Editor at Big for MINING.COM and Head of Adamas Within, supplying information and evaluation based upon Adamas Knowledge information.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/chart-price-spike-doubles-value-of-cobalt-ev-battery-market/