Increasing area steel costs are establishing among the greatest revenues years in current memory for varied miners, with Rio Tinto (ASX: RIO, LON: RIO) and Glencore (LON: GLEN) baiting upside possibility, according to a record by Bloomberg Knowledge

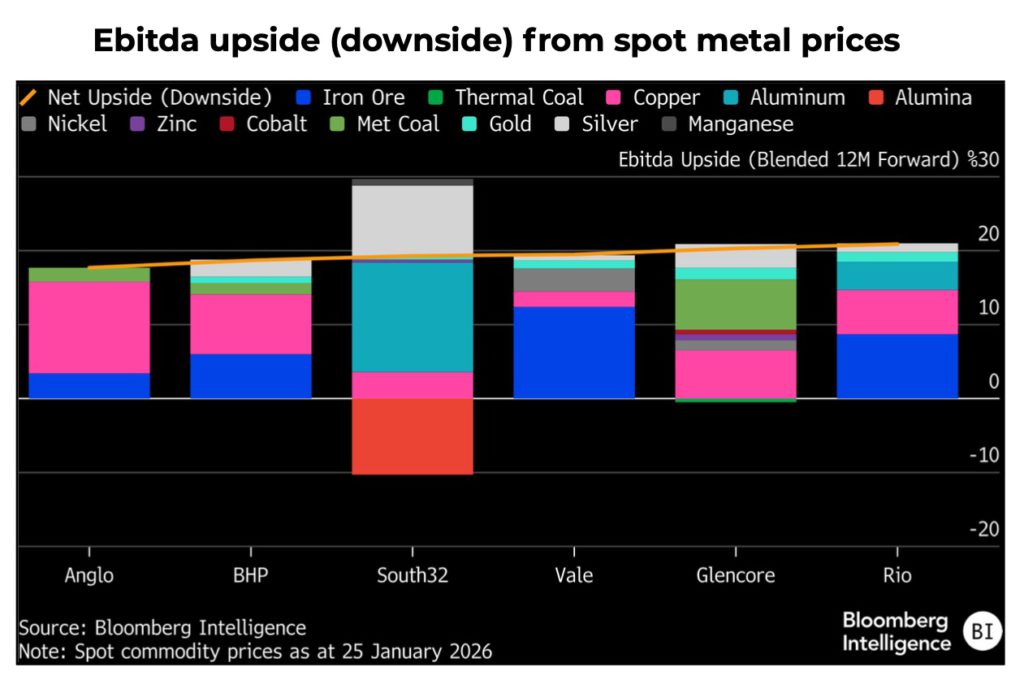

Area costs indicate 18%– 21% advantage to 1 year onward agreement Ebitda throughout significant varied miners if present degrees hold, noting the biggest revenues upside because very early 2025. Bloomberg Knowledge states Rio Tinto and Glencore display best, with about 20%– 21% upside suggested.

” Significant miners’ agreement Ebitda upgrades ought to speed up, led by Rio Tinto and Glencore,” claimed Alon Olsha, elderly sector expert at Bloomberg Knowledge, including that more powerful revenues modifications can sustain much more scrip-funded M&A however likewise increase implementation danger, especially for Rio.

Quality issues

The structure of revenues development matters as high as its dimension, with capitalists most likely to put a greater worth on advantage driven by copper and rare-earth elements than by iron ore, where agreement still thinks softer prices.

For Glencore, solid metallurgical coal and copper costs make up regarding two-thirds of its spot-implied Ebitda upside, while silver and gold include greater than 4% in spite of not being core revenues motorists.

Rio Tinto has actually seen especially solid revenues energy, with agreement projections raising its 2026 Ebitda by 18% over the previous 6 months, well in advance of peers, while area costs still indicate a more 21% advantage. That reinforces Rio’s loved one placement however elevates bench for any type of huge, scrip-funded procurement as revenues upgrades progressively show self-help and copper direct exposure.

By comparison, Glencore’s 2026 Ebitda has actually increased simply 5% over the exact same duration, recommending better extent for favorable modifications if area costs linger.

From Dr. to King

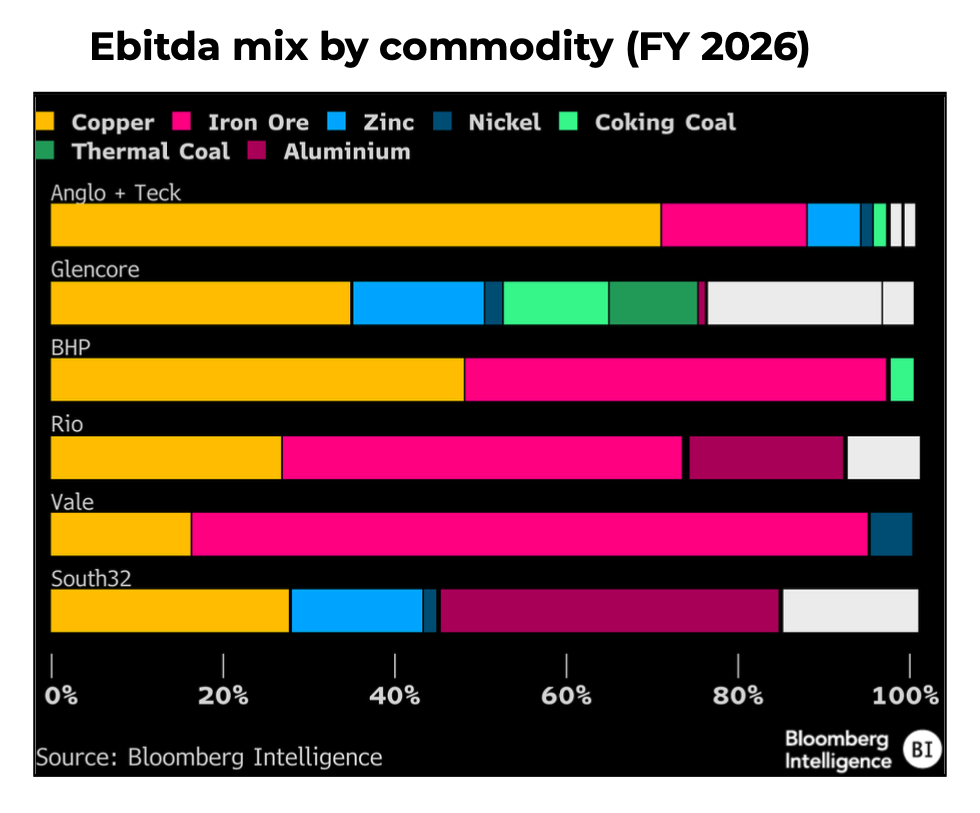

Copper’s growing dominance is improving the field’s revenues mix, changing the previous “Dr. Copper” right into what Bloomberg Knowledge currently calls the king of assets. Copper is readied to make up greater than 35% of varied miners’ Ebitda in 2026, up regarding 14% from 8 years earlier, driven greatly by greater costs and profile simplification instead of quantity development.

Rio Tinto sticks out on manufacturing, having lifted copper output by 54% since 2019 with the ramp-up of Oyu Tolgoi, compared to an 11% rise at BHP (ASX: BHP, LON: BHP). The race to safeguard copper-heavy pipes has actually escalated, pressing miners towards natural development and M&A prior to possessions are totally de-risked and rerated.

Anglo American’s (LON: AAL) transaction with Teck has actually increased its change towards copper, with pro-forma revenues readied to surpass 70% from the steel, complied with by BHP at virtually 50% and Glencore at regarding 35%. Rio’s copper direct exposure has actually increased with continual financial investment however still routes peers at about 26%, with iron ore controling at 47%.

Bloomberg Knowledge anticipates varied miners’ Ebitda to increase throughout the board in 2026, led by Glencore and Anglo at 24– 28% development.

Copper continues to be the vital bar, with costs seen increasing 25% versus 2025 under Bloomberg Knowledge’s circumstance, or around 16% on agreement, while Glencore’s advertising department includes upside if volatility remains high.

Greater costs likewise bring price dangers, especially work, however, for miners with rare-earth elements spin-offs, more powerful silver and gold costs ought to greater than countered those stress.

Roadway in advance

Implementation will certainly specify the year as miners press significant tasks onward. Glencore should supply cleaner operating efficiency while progressingCoroccohuayco and the Alumbrera restart Anglo deals with a vital stage finishing its Teck merging and streamlining its profile. BHP needs to steady Jansen, clarify its Australian copper method and supply the Vicuna technological research study in the initial quarter. Rio Tinto will certainly concentrate on lithium combination, progressing in-flight tasks and ending its minerals section calculated testimonial, while Vale (NYSE: VALE) proceeds deal with its strategy to increase copper result by 2030.

Macro patterns favour base steels over mass assets, with durable need from electrification, AI and protection investing, along with supply restraints and anticipated rates of interest cuts. Iron ore deals with a harder expectation as supply development speeds up and Chinese steel exports come across increasing worldwide profession obstacles.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/copper-rally-boosts-2026-earnings-outlook-for-miners-report/