Copper is heading right into an architectural shortage from 2026 as need from electrification speeds up faster than brand-new supply, according to BloombergNEF, with geopolitical treatment currently the solitary greatest pressure forming steels markets.

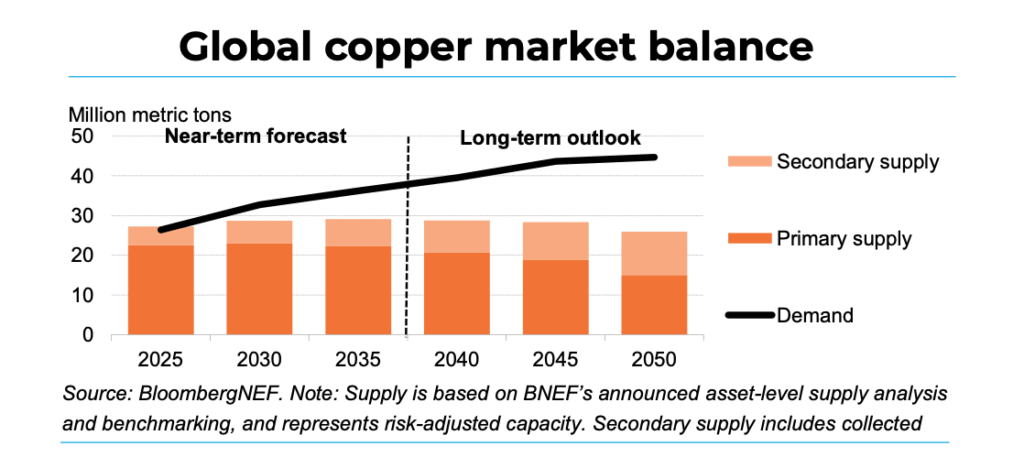

In its December record, Transition Metals Outlook 2025 BloombergNEF states copper deals with one of the most intense stress amongst change steels, driven by fast development in information centres, grid growth and electric-vehicle fostering. Energy-transition need for copper is readied to three-way by 2045, pressing the marketplace right into consistent shortage unless financial investment and reusing increase.

Kwasi Ampofo, head of steels and mining at BloombergNEF, informed MINING.COM the discrepancy shows climbing need hitting sluggish task distribution. “Copper, platinum and palladium have actually experienced really sluggish ability enhancement at once where need is expanding,” he claimed, calling them the assets under the best near-term stress.

Supply restraints are currently noticeable. Disturbances in Chile (Quebrada Blanca, El Teniente), Indonesia (Grasberg) and Peru (Las Bambas, Constancia), coupled with sluggish allowing, have actually tightened up the marketplace. BloombergNEF approximates the copper deficiency can get to 19 million tonnes by 2050 without brand-new mines or considerable gains in scrap collection.

Temporary rate relocations

Costs are up 35% so far this year and going to their biggest gain considering that 2009. While the copper-shortage discussion typically obscures temporary rate relocations with long-lasting basics, Ampofo claimed BloombergNEF’s overview is based in architectural supply-demand patterns. Bringing brand-new supply online this years will certainly need continual financial investment to increase existing jobs, structured allowing and much better reusing systems.

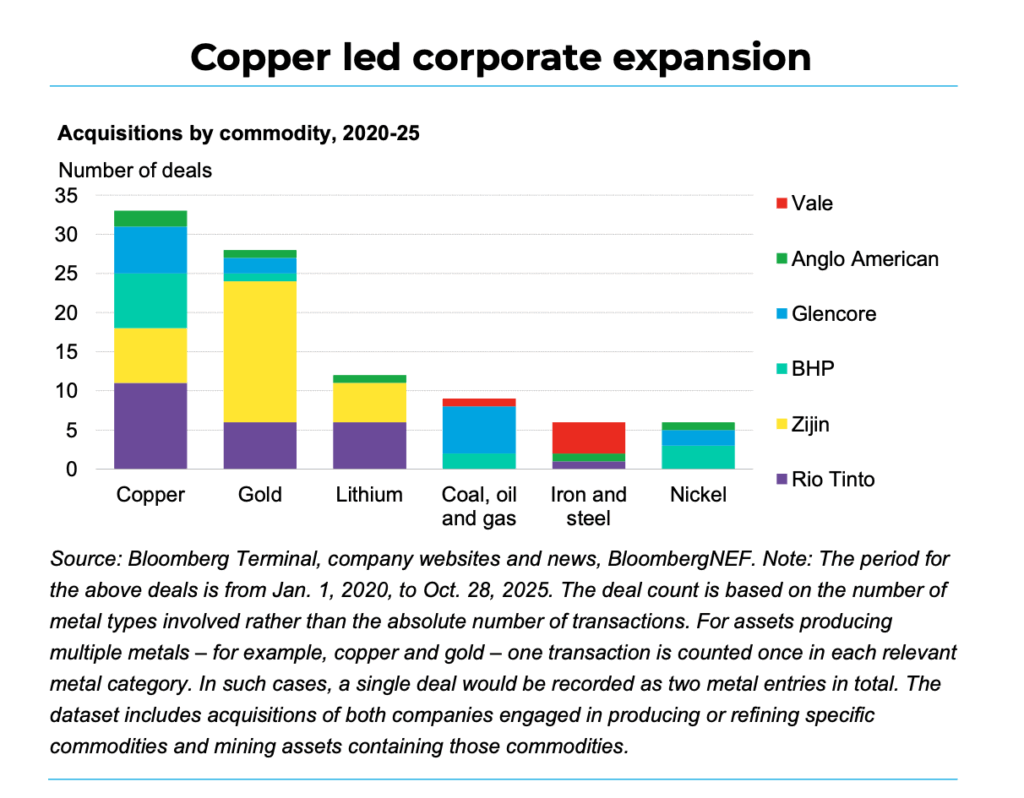

That long-lasting sight is significantly shared by miners. BloombergNEF notes restored capital investment and loan consolidation throughout manufacturers consisting of Anglo American (LON: AAL), BHP (ASX: BHP), Glencore (LON: GLEN), Rio Tinto (ASX: RIO), Vale (NYSE: VALE) and Zijin (HKEX:2899). Ampofo claimed the rise in mergings and procurements signals copper’s expanding tactical worth, a final thought the company’s evaluation sustains.

The others

While copper controls near-term problems, the record highlights splitting courses throughout various other steels.

Aluminium supply continues to be greatly focused in China, which generates half the globe’s result. A federal government cap focused on suppressing discharges has actually left little area to expand, and BNEF states the ceiling’s restraint on supply can linger unless elevated. China’s share decreases to 37% by 2050 in the Economic Shift Situation, while India greater than increases manufacturing over the following years.

Graphite need increases from 2.7 million tonnes in 2025 to 6.7 million tonnes in 2050, driven by its main duty in lithium-ion battery anodes. The marketplace is anticipated to get on technological shortage in 2032 as second supply from retired batteries stops working to match the stagnation in primary-supply development.

Lithium supply, by comparison, remains to expand. Complete ability can strike 4.4 million tonnes of lithium carbonate matching by 2035, up from 1.5 million tonnes in 2025, sustained by brand-new South American and African jobs, growing direct-extraction innovations and climbing second supply. Costs continue to be reduced after dropping from a 2022 height of $80,000 per tonne, though current interruptions and aid decreases have actually set off a small healing.

Manganese supply continues to be extensively straightened with need with 2050 many thanks to steady ore accessibility and leading usage in steelmaking, which makes up 97% of intake. Temporary dangers linger as a result of logistics obstacles in South Africa and Gabon’s intended 2029 export restriction.

Cobalt costs have actually recoiled after the Autonomous Republic of Congo enforced a four-month export restriction in February, later on changed with an allocation system that caps yearly exports at 96,600 tonnes for 2026– 27, a 50% cut from 2024 degrees. Costs climbed up 128% from February to October as the marketplace tightened up.

China’s prominence

In spite of wide financial investment in critical-minerals supply chains, China maintains prominence throughout a lot of midstream refining, particularly in aluminium, graphite, manganese, cobalt, nickel and unusual planets. Europe and the United States continue to be greatly subjected in graphite, manganese, nickel and lithium, while Japan and South Korea rely upon varied imports and reusing.

Geopolitics currently underpins much of those approaches. Ampofo claimed federal government participation can open funding yet additionally increases the threat of problem, and advised that aids alone will certainly not solve supply-chain focus. Looking in advance, he claimed rate signals in 2026 will certainly be vital, either urging brand-new supply or suppressing need with replacement.

The record additionally emphasizes the demand to decarbonize steels utilized in clean-energy facilities. Steel, aluminium and copper bring the greatest symbolized discharges, and while solar and wind jobs counter those discharges within months of procedure, BloombergNEF warns that sluggish development upstream can extend the carbon repayment duration.

发布者:Cecilia Jamasmie,转转请注明出处:https://robotalks.cn/coppers-next-shortage-is-structural-not-hype-analyst/