Copper’s record-breaking 2025 has actually established a limited yet delicate market heading right into 2026 as supply stress strengthen, toll anxieties misshape profession circulations and experts flag long-lasting shortages.

With just a couple of trading days left in the year on the London Steel Exchange, copper is up almost 40%, noting its biggest yearly gain considering that 2009. They rose past $11,800 a tonne this year, at one factor resting concerning 3% over any type of previous high as investors hurried steel right into the United States in advance of feasible Trump management tolls as high as 15%.

Expert Albert Mackenzie of Standard Minerals informed MINING.COM the company approximates that around 730,000 to 830,000 tonnes were drawn away right into United States storage facilities simply in October this year, swelling CME supplies while tightening up the remainder of the globe and driving costs greatly greater.

” We make use of the term ‘financially caught’ to describe that copper as the existing arbitrage and costs atmosphere implies there is no motivation for that product to be eliminated from the United States,” Mackenzie claimed. “This trapped tonnage is likely greater currently as product remains to stream right into the United States.”

Mackenzie kept in mind that while the copper cost has actually had a disorderly year, the rally appeared to have actually wandered away from principles. He included that the rise has actually been driven as a lot by toll hedging and an “EV– AI– power shift” financial investment story as by real supply deficiency.

The specialist recommends mining business have actually been so reliable at advertising the concept of an impending deficiency that financiers and investors have actually valued in future scarcities too soon, adding to greater costs today despite the fact that physical rigidity is unequal or otherwise yet serious.

” Mining business are pressing an engaging long-lasting scarcity story– and the marketplace thinks it,” Mackenzie claimed. “However idea and principles aren’t the very same point.”

The expert’s sight is that the long-lasting is undoubtedly favorable. Today is a lot more difficult. Much of the drawn away steel is being in storage space and leveraged versus the CME ahead contour instead of being eaten, Mackenzie kept in mind.

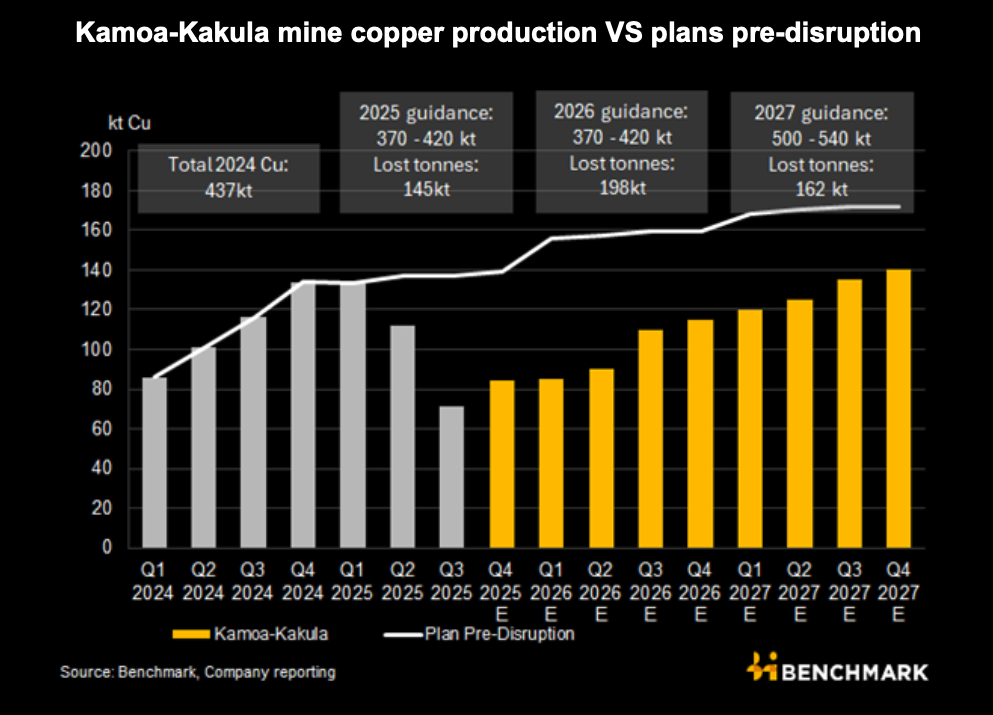

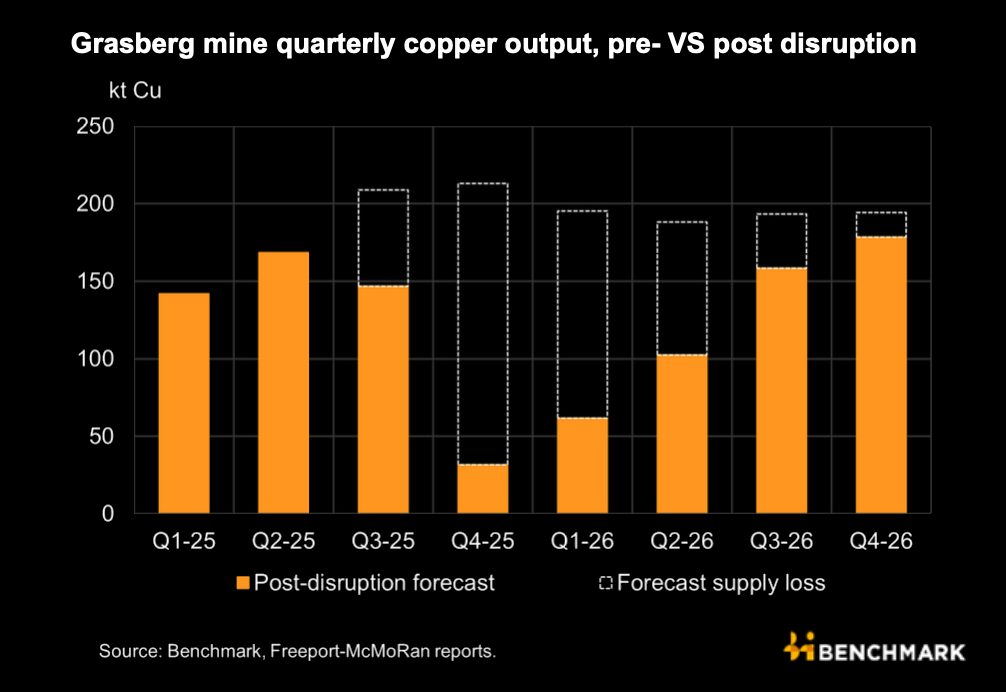

Hidden supply troubles included stress. Lengthy interruptions at Grasberg in Indonesia, Kamoa-Kakula in the DRC and Chile’s El Teniente extended with the year, with some mines not expected to recover 2024 result degrees till 2027 or later on.

Also procedures devoid of official interruptions fought with decreasing ore qualities, intricate geology or sluggish ramp-ups, leaving smelters pressed by limited concentrate accessibility.

Disturbances at Teck’s (TSX: TECK.A, TECK.B)( NYSE: TECK) QB2 project in Chile, and worse-than-recent production at mines consisting of Collahuasi, Los Bronces and a handful of various other mines contributed to the story of supply disturbance, Mackenzie claimed.

Solid theoretically, softer on the ground

Need development continued to be solid theoretically, backed by assumptions for electrical automobiles, grid upgrades, information centres and wider electrification. However near-term intake delayed the story, especially in China, where building and construction and components of producing remained soft. High costs pushed some buyers towards less expensive choices, though experts claimed the marketplace was limited instead of damaged.

Copper’s duty as a macro measure guaranteed plan and financial view drove sharp swings. Rates damaged greater when expect a China– United States profession bargain boosted, and investors responded rapidly to changes in stimulation assumptions. Any kind of brand-new Trump-era tolls on copper or copper-heavy devices might shake circulations and need, including an additional layer of volatility throughout the LME– CME spread, experts alert.

Alternative and scrap functioned as safety and security shutoffs. Designers took another look at light weight aluminum in circuitry applications when copper traded much over it, and high costs attracted a lot more ditch right into flow. While not smooth, these stress can cover rallies if need begins to deteriorate.

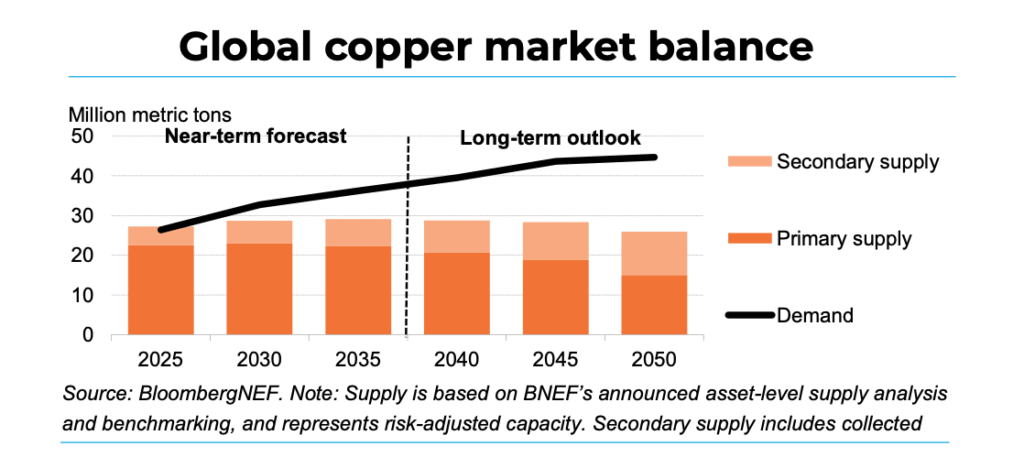

Longer term, experts see much deeper architectural dangers. BloombergNEF‘s December Transition Metals Outlook 2025 advises copper need for the power shift might triple by 2045 which the steel might get in architectural deficiency as very early as 2026. Disturbances in Chile, Indonesia and Peru, in addition to sluggish allowing and a weak pipe of brand-new mines, intensify the space. Without significant financial investment in brand-new jobs and reusing, the deficiency might get to 19 million tonnes by 2050.

Kwasi Ampofo, head of steels and mining at BloombergNEF, told MINING.COM earlier this month the forecasted copper market discrepancy shows increasing need hitting sluggish job shipment. “Copper, platinum and palladium have actually experienced really sluggish capability enhancement each time where need is expanding,” he claimed, calling them the products under the best near-term stress.

Various other essential minerals encounter their very own restraints. Light weight aluminum development is restricted by China’s manufacturing cap, graphite need is anticipated to climb up towards a technological deficiency by 2032, and cobalt costs have actually recoiled after the DRC changed its export restriction with an allocation reducing deliveries by 50% for 2026– 27.

Lithium supply remains to increase, yet costs stay much listed below their 2022 optimal. Throughout manufacturers, consisting of Anglo American (LON: AAL), BHP (ASX: BHP), Glencore (LON: GLEN), Rio Tinto (ASX: RIO), Vale (NYSE: VALE) and Zijin (HKEX:2899), capital investment is increasing as business chase after future supply.

What to look for in 2026

Taken with each other, 2025 exposed a copper market tighter than in previous cycles, yet not yet in the architectural scarcity frequently promoted. Virtually one million tonnes of copper might be parked in United States storage facilities without evident physical scarcities in other places, also at document costs. At the very same time, the long-lasting restraints on brand-new supply and the expanding copper strength of the international economic climate are actual.

For 2026, viewers anticipate even more of the very same: a market drew in between a really favorable long-lasting tale and an extra jumbled near-term truth, with tolls, profession plan and macro information driving sharp swings. In copper, the deficiency might still be in advance, yet the volatility is currently right here.

The vital variables, they concur, are profession streams right into the United States, recuperation at significant mines and the international financial expectation.

If investors remain to draw away thousands of hundreds of tonnes to CME-deliverable storage facilities in advance of prospective tolls, rigidity in the remainder of the globe will certainly linger and costs will certainly stay raised, experts state.

A toll shock might send out costs turning in either instructions, while fresh interruptions or hostile Chinese stimulation might rapidly improve equilibriums. Experts anticipate high costs to linger yet with much deeper adjustments if replacement and scrap speed up.

” As long as Donald Trump stays in the White Residence, markets ought to support for even more abrupt swings triggered by plan changes or off-the-cuff comments– impacts that prolong well past copper itself,” Mackenzie wrapped up.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/coppers-tight-supply-and-tariff-risks-set-for-a-volatile-2026/