Cobalt rates have actually dropped to their cheapest degree because 2016, as a deluge of supply bewilders going stale need from the electrical lorry market.

Area rates for the steel dropped to simply over $11 an extra pound ($ 24,300 per tonne) recently contrasted to optimals over $40 an extra pound in 2018 and once more in 2022.

Cobalt sulphate (minutes. 20.5% cobalt supplied) entering the EV battery supply chain in China standards 26,500 yuan or $3,655 per tonne in January, below optimals of over $20,000 and $18,000 a tonne in 2018 and 2022, specifically.

In a current note, BMO Funding Markets explained that actually actual cobalt rates go to the most affordable in background based upon yearly ordinary rates changed for rising cost of living returning to the late 1920s making use of USGS information.

Almost all cobalt outcome is a by-product of nickel and copper mining. Copper manufacturing in the Congo is increasing quickly resulting in a close to 40% enter the nation’s cobalt outcome in 2024. The DRC currently makes up 80% of worldwide cobalt supply, approximated to have actually gone beyond 300,000 tonnes in 2024.

Cobalt result outcome is likewise boosting in Indonesia, in charge of majority the globe’s nickel supply after years of development.

BMO states there is no assistance to quit rates from dropping additionally with rates collapsing via the historic flooring offered by little range swing vendors:

” Cobalt is familiar with excess, and at this moment we would commonly see the marketplace harmonizing by means of the decrease in artisanal outcome in the DRC. Nonetheless, the cobalt market is currently so huge that it can not be stabilized by the elimination of artisanal mining alone.”

BMO has actually not discovered sufficient proof to recommend smaller sized DRC manufacturers have actually started turning off their cobalt circuits and thinks federal government tactical stockpiling is not adequate to take in supply and just indicators of cobalt tailings development (to be recuperated if and when rates enhance) would certainly recommend a rate flooring has actually been gotten to.

On the need side, the overview is likewise much from glowing.

The EV market is still broadening at a healthy and balanced clip and 2025 will certainly probably be the very first fiscal year that complete guest EV battery ability implementation– a much better indication battery products need than system sales alone– surpasses 1 terawatt hours according to Adamas Knowledge, a Toronto-based EV supply chain research study company.

This would certainly comprise a various globe than 2017 when the after that biggest cobalt manufacturer Glencore first touted the coming boom for cobalt from the incipient EV market. That year 38 GWh of EV battery power rolled onto the world’s freeways and byways.

While cobalt usage in EV batteries, the resource of the mass of cobalt need, remains to climb, it is well listed below the blue-sky projections made not that lengthy back.

The marketplace share of cobalt-free batteries such as lithium iron-phosphate, or LFP, remains to broaden swiftly. In China, the share of LFP on a GWh basis was 65% in November, one of the most current month with thorough information.

At the very same time, per lorry cobalt usage in NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminium) batteries is likewise wandering reduced because of recurring thrifting and a fad in the direction of high-nickel cathodes (much less than 10% cobalt), especially in markets outside China.

The truth that Chinese car manufacturers are lengthening their use mid-nickel batteries (approximately 50% nickel, 20% cobalt and 30% manganese) due to the fact that the price space to LFP has actually tightened considerably gives just chilly convenience.

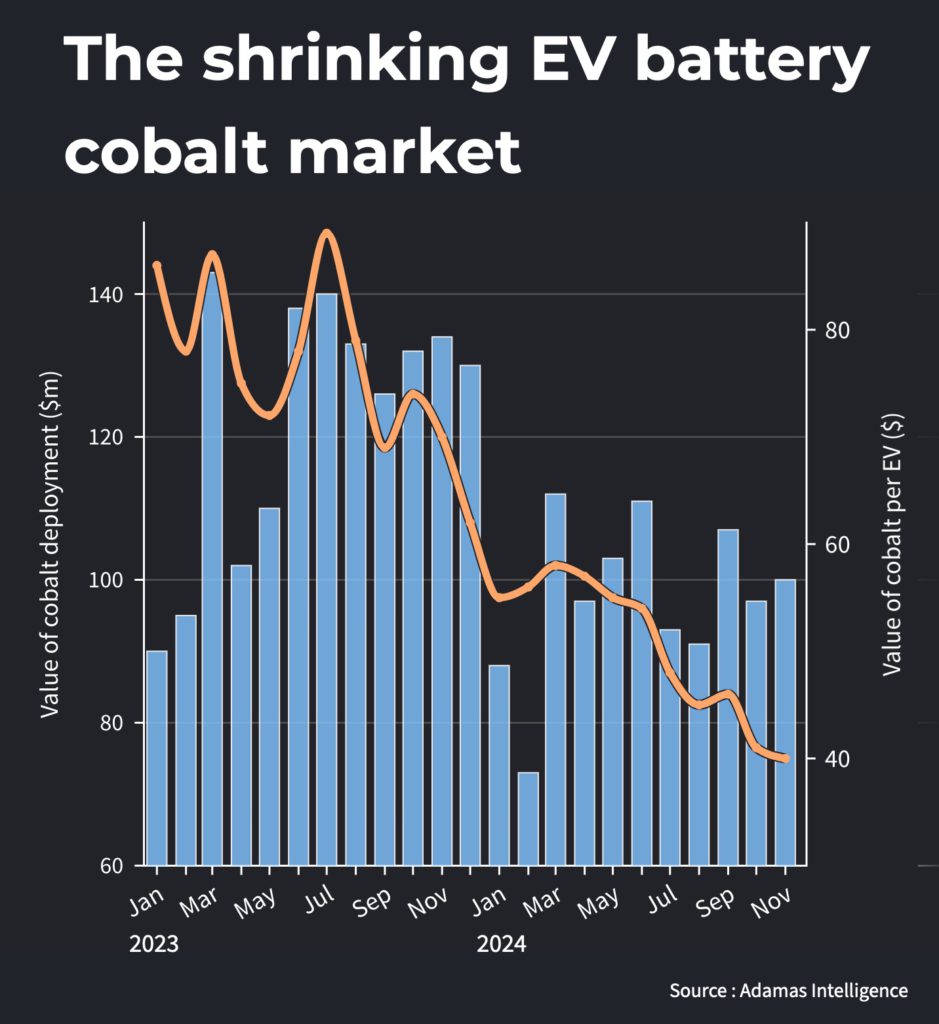

The most up to date information from Adamas Knowledge tracking EV sales, battery ability and chemistry in over 110 nations coupled with month-to-month rates reveals the dimension of the battery cobalt market is lessening swiftly also as the complete included tonnes in newly-sold EVs boost.

Throughout 2021, when the electrification of the worldwide vehicle parc got to 286 GWh, according to Adamas Knowledge information, the worth of cobalt discovered in the battery packs of EVs marketed that year involved $1.9 billion (and in the list below year expanded by one more $540 million).

In 2015 that number was to $1.2 billion regardless of the set up cobalt tonnage having actually increased because 2019 to simply shy of an approximated 60,000 tonnes (bearing in mind that these are incurable set up tonnes and do not think about return losses throughout conversion, refining and production).

As the chart reveals the analysis of cobalt product prices on a sales-weighted ordinary basis is a lot more alarming. Every EV marketed worldwide, consisting of plug-in and standard crossbreeds, currently standards simply over $40 well worth of cobalt. That number came to a head in March 2022 at $260.

For a fuller evaluation of the EV battery steels market check out the February issue of the North Miner print and electronic versions.

* Frik Els is Editor at Huge for MINING.COM and Head of Adamas Within, giving information and evaluation based upon Adamas Knowledge information.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/graph-cobalt-price-plunge-and-the-ev-market/