In 2015, copper mining market viewers were maintained amused by the potential customers of a tie-up in between BHP and Anglo American after the globe’s leading miner in Might introduced an unwanted quote for the 108-year old firm.

The FT reported over the weekend break that Melbourne-based BHP is placing a proposal for Anglo on ice. Not unusual offered the aberration in their share rate efficiency and whether BHP has the pockets or the belly for a currently much more expensive acquisition has actually constantly remained in question.

Anglo American greater than when rejected BHP’s breakthroughs, yet given that the sweetened $49 billion requisition was initial declared dead, the London-headquartered firm has actually been hectic getting in the right shape ought to BHP have another go (still not eliminated completely, offered the firm’s mindful phrasing around the problem).

Anglo is dumping its Southerly African ruby and platinum, Australian coal and Brazilian nickel properties.

The restructuring along the lines required by BHP in its initial technique and would certainly see copper comprise 60% of Anglo’s profile. With each other the miners would certainly generate 1.9 million tonnes of copper on an attributable basis.

BHP is currently rotating to natural development with approximately $10bn being invested in Escondida alone, the globe’s biggest copper mine, in which Rio Tinto has a 30% risk.

Talks in between Glencore and Rio Tinto held late in 2015 and exposed in January show up to have actually delayed, yet the incentive for huge mergings on top of mining lives and well.

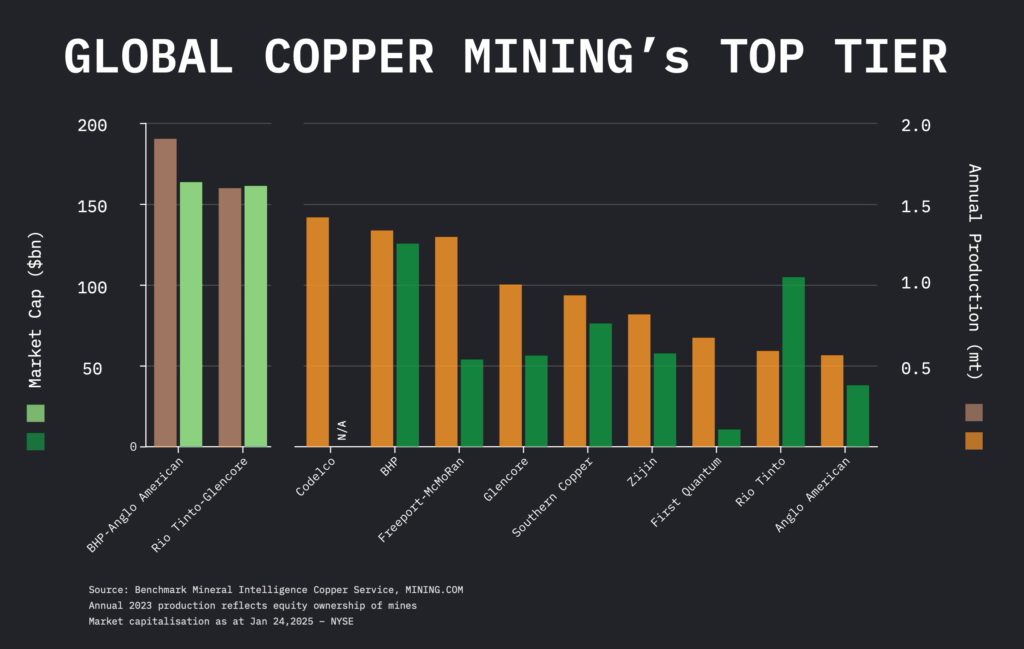

Based upon today’s market assessment, a BHP-Anglo mix would certainly deserve some $160 billion, practically on the same level with that said of a joined Glencore and Rio Tinto.

Incorporated copper manufacturing on an equity basis would certainly drop well except BHP-Anglo at 1.6 m tonnes, nonetheless.

Need to these mixes occur 16% of worldwide copper manufacturing would certainly be managed by simply 2 business. As it stands the business detailed in the coming with chart stand for almost 40% of the worldwide overall.

In a note, Criteria Mineral Knowledge’s copper service states under a Glencore-Rio Tinto merging the capacity for copper manufacturing development is significant, and is mostly driven by the latter’s properties.

Need to Rio Tinto’s Resolution task in Arizona in some way be reanimated– and with Trump back in workplace those chances have improved— the position of leading manufacturers would certainly not alter a lot, nonetheless. Rio Tinto has a 55% risk and BHP has the rest of what can be a 450,000 tonnes annually mine.

Criteria mentions that Oyu Tolgoi in Mongolia, which is 66% possessed gets on track to accomplish manufacturing of 500,000 of copper by the end of the years, with the below ground growth advancing gradually. Escondida is forecasted to get to peak manufacturing of 1.3 Mt of copper in 2025, yet additionally supplies substantial brownfield growth chances.

Glencore additionally brings tonnes to the table.

Criteria states the firm’s standout property is its 44% risk in Collahuasi, a mine with a 76-year life-span and substantial growth capacity.

2 huge mines with cobalt spin-offs and critical operating experience in the Congo additionally matter in Glencore’s favour, especially since Western federal governments are belatedly rediscovering Africa as a possible vendor of essential minerals and worldwide profession is quick returning to its mercantilist origins.

The DRC has actually been the primary resource of added copper tonnes beginning stream for 4 out of the last 5 years and the main African country is most likely to include one more 200,000-plus to annual extracted copper in 2025.

Glencore additionally has a considerable greenfield profile in Latin America with tasks such as West Wall Surface, El Pachón, and MARA each having the possible to become significant copper mines in the years ahead, states Criteria.

Baar-based Glencore is always looking for deals.

In 2014, Glencore under previous chief executive officer Ivan Glasenberg, hardly 2 years after gobbling up Xstrata for $90 billion to include a huge mining profile to its after that high-flying trading service, made its initial effort to combine with Rio Tinto.

That technique was a non-starter in Melbourne, yet with ever before even more laden geopolitics, Glencore’s abilities at browsing the worldwide products profession might become far more of a possession this time around around. At $228 billion a year, Glencore’s earnings overshadows those of its peers, and it has actually never ever hesitated to toss its weight around.

Glencore made a not successful $23 billion quote for Teck Resources in 2023 yet did wind up with the Vancouver-based firm’s coal properties.

Under pressure from shareholders, Glencore is clinging onto its really lucrative coal mining and trading service, yet with Rio Tinto well promoted departure from the market, the nonrenewable fuel source might well be an overwhelming merging challenge for its green-conscious investors.

Teck would certainly’ve included a web 360,000 tonnes to Glencore’s yearly copper result, yet Teck is itself on an aggressive copper growth path promising to up manufacturing to 800,000 tonnes which also on a possessed basis would certainly put the firm strongly amongst the leading 10 manufacturers.

One more dark equine in copper M&A is Very first Quantum Minerals. Recently the Vancouver-based firm dissatisfied markets with a cut to its 2025 production guidance.

Very first Quantum is targeting 400,000 tonnes this year, yet if and when its Cobre Panama mine is rebooted (agreement appears to be late this year or initial fifty percent of 2026) the firm’s payment to worldwide copper manufacturing can go beyond that of Anglo.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/graph-what-global-copper-minings-top-tier-could-look-like/