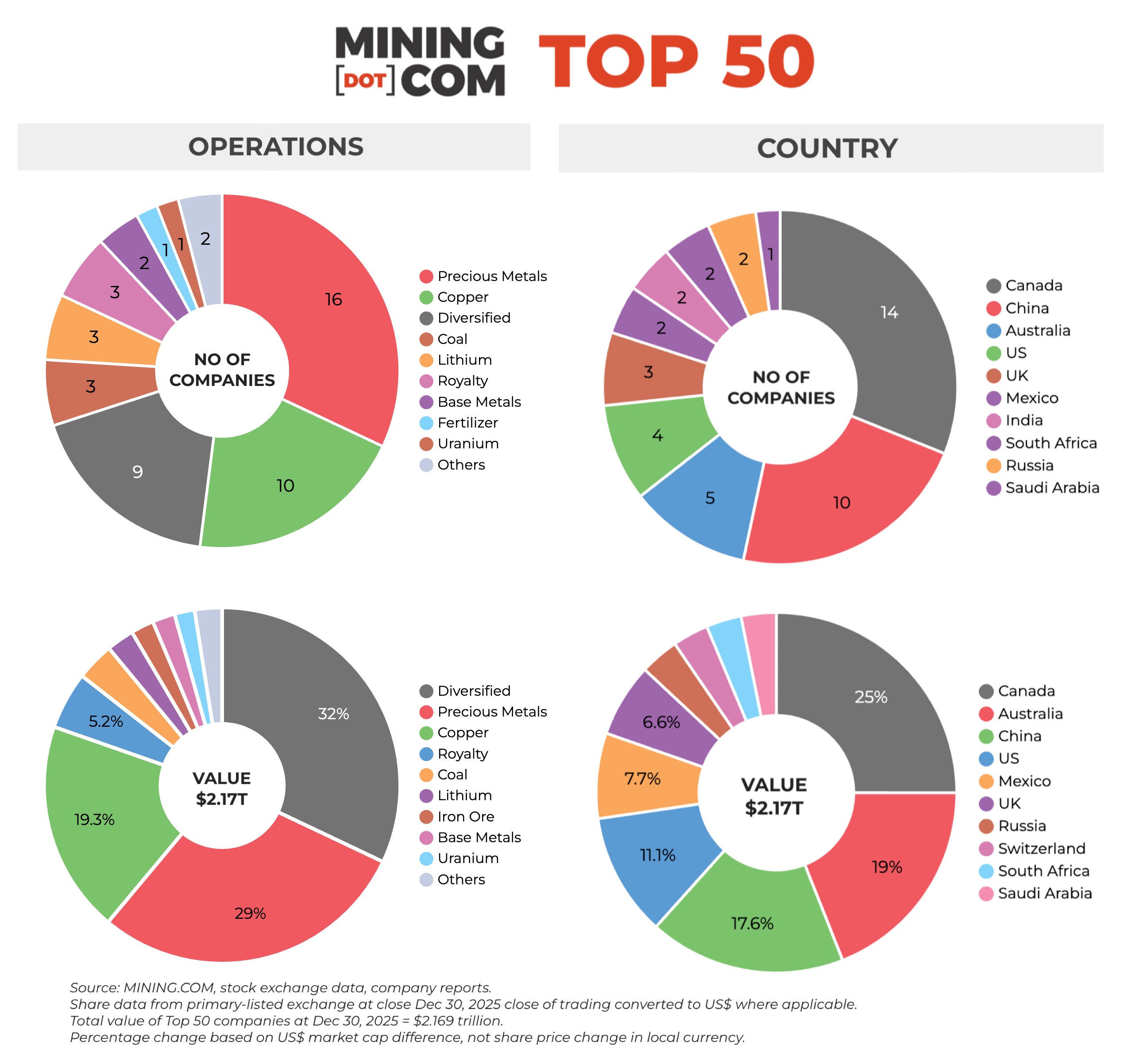

At the end of the 4th quarter the MINING.COM TOP 50 * position of the globe’s most important miners had a consolidated market capitalization of $2.17 trillion, up an amazing $892 billion in 2025.

A lot of the gains gathered in the 2nd fifty percent and after 3 years of torpidity, the marketplace evaluation of mining and steels shows up to have actually lastly overtaken various other fields. The foundation of the worldwide commercial economic situation are lastly seen wherefore they are: crucial.

From lip solution (not even), Western federal governments (the United States specifically) are currently placing cash behind mining, reaching an affordable method China has actually effectively utilized because the millenium.

The position is based upon a business’s market capitalization in neighborhood money on its key exchange and after that transformed to USD so the near-double figure decrease in the dollar this year provided some assistance to supply and products costs. Yet a rerating of the market has actually been long overdue.

A lot of the credit history for the 70% enter the worth of the Leading 50 can most likely to widespread rare-earth elements costs and copper, however gains have actually been broad-based and also old-economy iron ore and much reviled lithium signed up with the celebration, albeit late.

The very best doing listing radiates with silver and gold counters consisting of a five-fold rise for Fresnillo, the London-listed silver miner managed by Mexico’s Peñoles, which has actually currently sealed its placement midway up the position after decreasing in and out for several years.

The rigid competitors to make the listing this year is shown by the destiny of Coeur Mining. After getting in the Leading 50 for the very first time at the end of September, a middling efficiency in Q4 saw the Chicago-based silver and gold miner befall of the ranking in spite of greater than tripling in worth throughout 2025.

Besides all points valuable and base, unusual planet was the standout tale of 2025. Perth’s Lynas Rare Planet squealed in at no 49 after at the end of Q3 to sign up with Las Vegas-based MP Products which soared up the graphes in the very first fifty percent after a cutting-edge manage the Government.

MP Products still reveal gains north of 200% for the year and Lynas has actually increased, however that was not nearly enough and currently both counters have actually befalled of the position once again, leaving just China Northern Rare Planet to stand for the 17 components as it has for years.

Replacing the unusual planet supplies are the globe’s 2 biggest lithium manufacturers. An increase to the cost of the battery steel in the 2nd as excess started to relieve, saw Chile’s SQM and United States manufacturer Albemarle go back to the Leading 50, bringing the variety of lithium miners back to 3.

The market came to a head in 2022 with 6 supplies in the ranking and Tanqi Lithium placed 58th presently might well join its Chinese equivalent Ganfeng if the lithium uptrend proceeds, however Australian manufacturers like Minerals Resources and Pilbara Minerals (currently PLS Team) might have a more challenging time of it.

Given that creation, the MINING.COM TOP 50 was headed by 2 companies — BHP and Rio Tinto– the only miners with regular market capitalizations over $100 billion (with a wobble here and there). Currently there are 5 companies with the difference.

With a string of purchases behind it, Chinese champ Zijin Mining, worth $124 billion after a 127% admiration only simply pipped Southern Copper, which has actually additionally started an aggressive expansion strategy, for 3rd, up 64% to $119 billion.

Southern Copper, the NYSE-listed mining arm of Grupo Mexico, was signed up with by Newmont in the triple digit club last quarter however unlike its acquisitive peers, soon after ingesting Australia’s Newcrest Mining for $17 billion, Denver-based Newmont started a multi-billion dollar divestiture program.

Agnico Eagle and Kirkland Lake Gold integrated in 2022 and the Toronto-based team remains to screw on possessions, making it a prospect for the $100 billion mark ought to gold proceed its gravity opposing rally. Agnico has actually increased in worth this year and deserves $86.3 billion.

Anglo and Teck Resources can yet become the largest mining bargain of the years since Ottawa has blessed the combination, many thanks in no tiny component to Anglo’s dedication to relocate its London head office to Vancouver.

Yet scaling the $100 billion degree might verify evasive. In spite of dual figure gains, both Teck and Anglo made the year’s worst entertainer listing– simply one more indicator what a wild adventure 2025 has actually been.

Anglo-Teck would rarely split the leading 10 with a consolidated worth of a color under $68 billion, however will certainly put it in advance of Swiss miner and products investor Glencore, which once more underperformed in 2025.

That would certainly rub salt in the wound for Baar, which attempted and fell short to get Teck a number of years earlier and is still trading, virtually 15 years later on, listed below its 2011 IPO price.

NOTES:

Resource: MINING.COM, stock market information, business records. Share information from primary-listed exchange on December 30, 2025 close of trading transformed to US$ where appropriate. Portion adjustment based upon US$ market cap distinction, not share cost adjustment in neighborhood money.

Just like any kind of ranking, standards for incorporation are controversial. We chose to leave out unpublished and state-owned ventures first as a result of an absence of details. That, certainly, leaves out titans like Chile's Codelco, Uzbekistan's Navoi Mining (the gold and uranium titan might provide later on this year), Eurochem, a significant potash company, and a variety of entities in China and establishing nations worldwide.

An additional main standard was the deepness of participation in the market, and just how much upstream is the mass of its earnings, prior to a venture can truly be called a mining business.

As an example, should smelter firms or product investors that possess minority risks in extracting possessions be consisted of, particularly if these financial investments have no functional part and even necessitate a seat on the board? This is an usual framework in Asia and omitting these kinds of firms eliminated popular names like Japan's Marubeni and Mitsui, Korea Zinc and Chile's Copec.

Degrees of functional or critical participation and dimension of shareholding were various other main factors to consider. Do streaming and aristocracy firms that get steels from mining procedures without shareholding certify or are they simply was experts funding lorries? We consisted of Franco Nevada, Royal Gold and Wheaton Rare-earth Elements on the basis of their deep participation in the market.

Up and down incorporated problems like Alcoa and power firms such as Shenhua Power or Bayan Resources where power, ports and trains compose a huge section of profits present a trouble. The earnings mix additionally has a tendency to alter together with unstable coal costs. Exact same goes with battery manufacturers like China's CATL which is progressively relocating upstream, however where mining will certainly remain to stand for a tiny section of its evaluation.

An additional factor to consider is varied firms such as Anglo American with individually detailed majority-owned subsidiaries. We have actually consisted of Angloplat (currently Valterra) to track PGM depiction in the ranking however omitted Kumba Iron Ore in which Anglo has a 70% risk to prevent dual checking. Likewise, we omitted Hindustan Zinc which is detailed individually however bulk had by Vedanta.

With various other teams like Mexico's Penoles where refining and chemicals compose a considerable component of business where feasible the Leading 50 would certainly consist of individually detailed running subsidiaries that are committed to mining. This is additionally why Southern Copper stands for Grupo Mexico in the position.

Several steelmakers very own and usually run iron ore and various other steel mines, however for equilibrium and variety we omitted the steel market, and keeping that numerous firms that have considerable mining possessions consisting of titans like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and numerous others.

Head workplace describes functional head office any place appropriate, as an example BHP and Rio Tinto are revealed as Melbourne, Australia, however Antofagasta is the exemption that shows the policy. We take into consideration the business's HQ to be in London, where it has actually been detailed because the late 1800s.

Please allow us recognize of any kind of mistakes, noninclusions, removals or enhancements to the ranking or recommend a various approach: e-mail Frik Els at fels@mining.com with Top 50 in the subject line.

.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/rerated-top-50-mining-companies-soar-past-2-trillion-valuation/