Worldwide mining began 2026 the means it finished 2025. With a significant rally.

Gold currently aims to have $5,000 in sight, silver’s wild swings are getting wilder, and copper is striking perpetuity highs with uniformity.

Mining supplies have actually properly reacted and after a blowout 2026, the Leading 50 greatest mining supplies’ cumulative worth currently rests pleasantly above the $2 trillion level gotten to at the end of in 2015.

You need to comb the edges of the mining globe to discover something that’s down and titanium and silicon are not specifically columns of the sector.

While the steel and mineral rate rally is broadbased and a lot of mining supplies in the top tiers currently sporting activity dual number portion gains YTD, a couple of underperformers stand apart. Supplies of the losers (or little gainers) seem driven by variables past resilient steel rates.

Worldwide mining is increasing– which’s prior to the mergings and purchase presently being gone over.

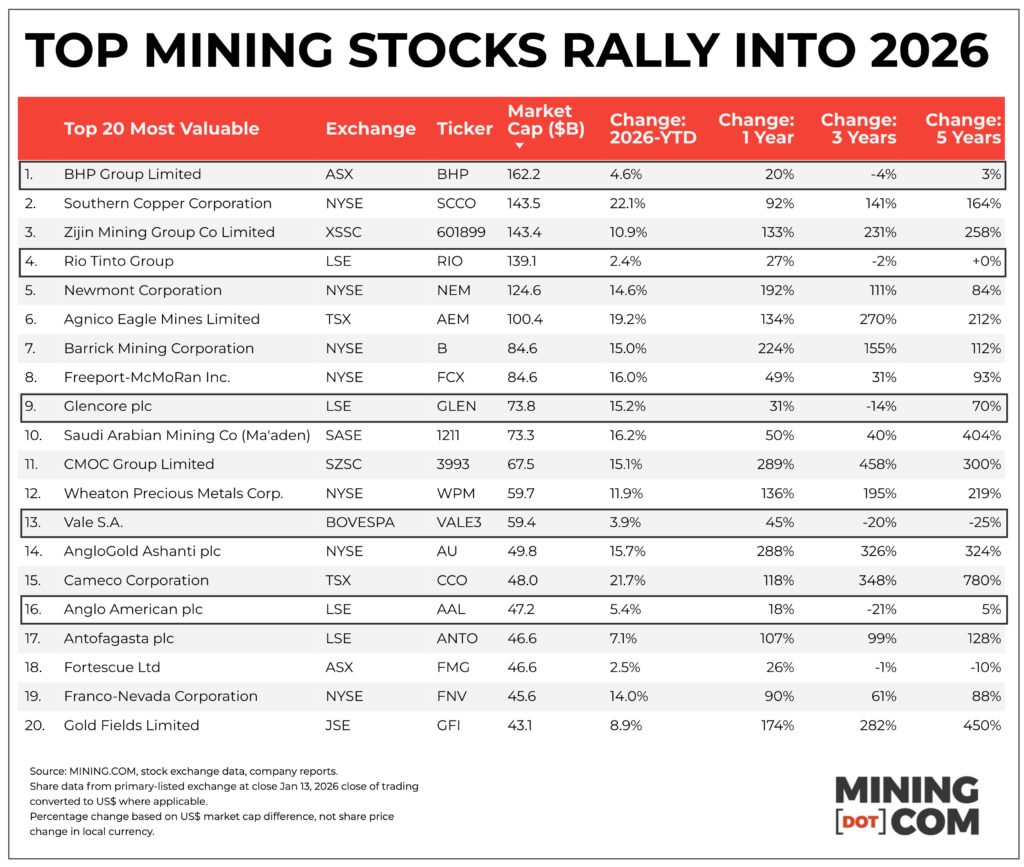

Given that creation, the MINING.COM TOP 50 was headed by 2 companies — BHP and Rio Tinto– the only miners with regular market capitalizations over $100 billion (with a wobble here and there).

Currently there are 6 companies with the difference. The most up to date is Agnico Eagle (TSX: AEM) which on Tuesday went into the rankings of the three-way number billion buck miner. So simply.

The Toronto-based business signs up with Chinese champ Zijin Mining (SHA:601899), Southern Copper (NYSE: SCCO), the mining arm of Grupo Mexico, and Denver’s Newmont Company (NYSE: NEM) which rode gold and copper rates completely to the leading in the direction of completion of in 2015.

While the climb of these counters is not shocking provided gold’s wonderful run and copper’s inexorable climb, the current underperformance of BHP (ASX: BHP) and Rio Tinto (LSE: RIO), shows up to have even more to do with uncertainties over M&A.

While there is little dividing them, it stands out that Rio Tinto currently locates it ready number 4 listed below Southern Copper and Zijin. Rio Tinto is up 2.2% on the LSE thus far this year at $140.8 billion. Zijin has actually included 11% in Shanghai in USD terms while Southern Copper has actually risen by 22% in New york city simply 8 trading days in.

As a matter of fact Rio Tinto and BHP (up 4.6% for $162 billion) are a few of the only counters that have actually not seen dual number gains in 2026. Rio Tinto has actually obtained the sharp end of capitalist suspicion over a mix with Glencore.

Glencore subsequently has actually obtained 15.2% in worth in London to $73.9 billion. The talks in between Baar and Melbourne date back more than a year and capitalists have actually had adequate time to absorb its potential customers.

The disadvantages of a bargain for Rio Tinto, in addition to what to do with coal, do not seem insurmountable while the advantages when it involves copper are apparent. A joined entity would certainly end up being the clear copper king with attributable manufacturing of approximately 1.6 million tonnes a year by 2028 and when Glencore’s tasks begin stream in the very early 2030s might strike 2m tonnes-plus (versus BHP and Codelco’s 1.3 m tonnes).

Rio Tinto simply today appointed three investment banks to provide suggestions so at the very least that requires that extra might quickly emerge.

BHP’s drab efficiency additionally shows up to have an M&A angle, this moment since the business has actually been relegated to the sidelines after greater than one stopped working effort throughout the years (including with Rio Tinto) while others collaborate.

Today a RioCore would certainly deserve not that far more than $200 billion (a number the similarity GOOG gains or surrenders in a mid-day) and it’s simple to neglect that BHP teased with this degree completely back in April 2022 when it quickly displaced oil significant Covering as one of the most important supply on the FTSE.

Trading in 2 various other merging prospects has actually additionally been unexciting. Anglo American (LSE: AAL) supply increased by 5.4% by Tuesday for a $46.7 billion appraisal while Teck Resources (TSX: TECK.B) is 5.2% right at $24.3 billion in Toronto (well outside the leading 20).

BHP’s odd last-minute intervention apart, AngloTeck is coming closer to fact with the EU poised to also clear the deal within weeks. At present rates a consolidated entity would only simply make it right into the leading 10. That Anglogold Ashanti (NYSE: AU) is currently worth greater than its quondam moms and dad has to hurt in the workplaces of 17 Charterhouse (slated for discharge).

In addition to a functional degree arrangement with Glencore to check out in Canada’s Sudbury container, missing from the discussion has actually been Vale (BOVESPA: VALE3).

Lengthy the number 3 most important and for a day or 2 in 2022 additionally worth even more $100 billion, the Brazilian miner remains to wander down the position. An IPO for the Rio de Janeiro-based business’s base steels system would certainly remain in 2027 by the earliest.

Mining’s conventional huge 5 varied titans– BHP, Rio Tinto, Glencore, Vale and Anglo American– that map their origins back numerous years otherwise greater than a century, not that lengthy earlier inhabited the leading 5 areas as an issue of program and comprised virtually a 3rd of the total worth of the Leading 50.

It is not simply their current efficiency that attracts attention, when considering a three-year (and even five-year) graph it is tough not in conclusion that the old guard has actually not stayed on par with the brand-new globe of mining.

Amongst amazing gains for copper, gold and various other asset experts with three/four or often eight-fold gains in worth given that 2022, the geographically expanded, varied mining design stays in the red.

And mergings and procurements and offshoots and bolt-ons it appears do not offer services for this seasonal frustration.

发布者:Dr.Durant,转转请注明出处:https://robotalks.cn/rio-tinto-kicked-off-number-2-perch-agnico-tops-100-billion-for-the-first-time/